When is Premium Riskier Than Loss?

Premium to GDP Ratio: 1968 Watershed

Premium to GDP Ratio

Premium to GDP Ratio: Cyclical Growth Between 1947 and 1997

The Underwriting Cycle Is Driven by Commercial Lines

Calm Surface Masks Inner Turmoil

Premium and GDP Growth Since 1992 (1992=1.0)

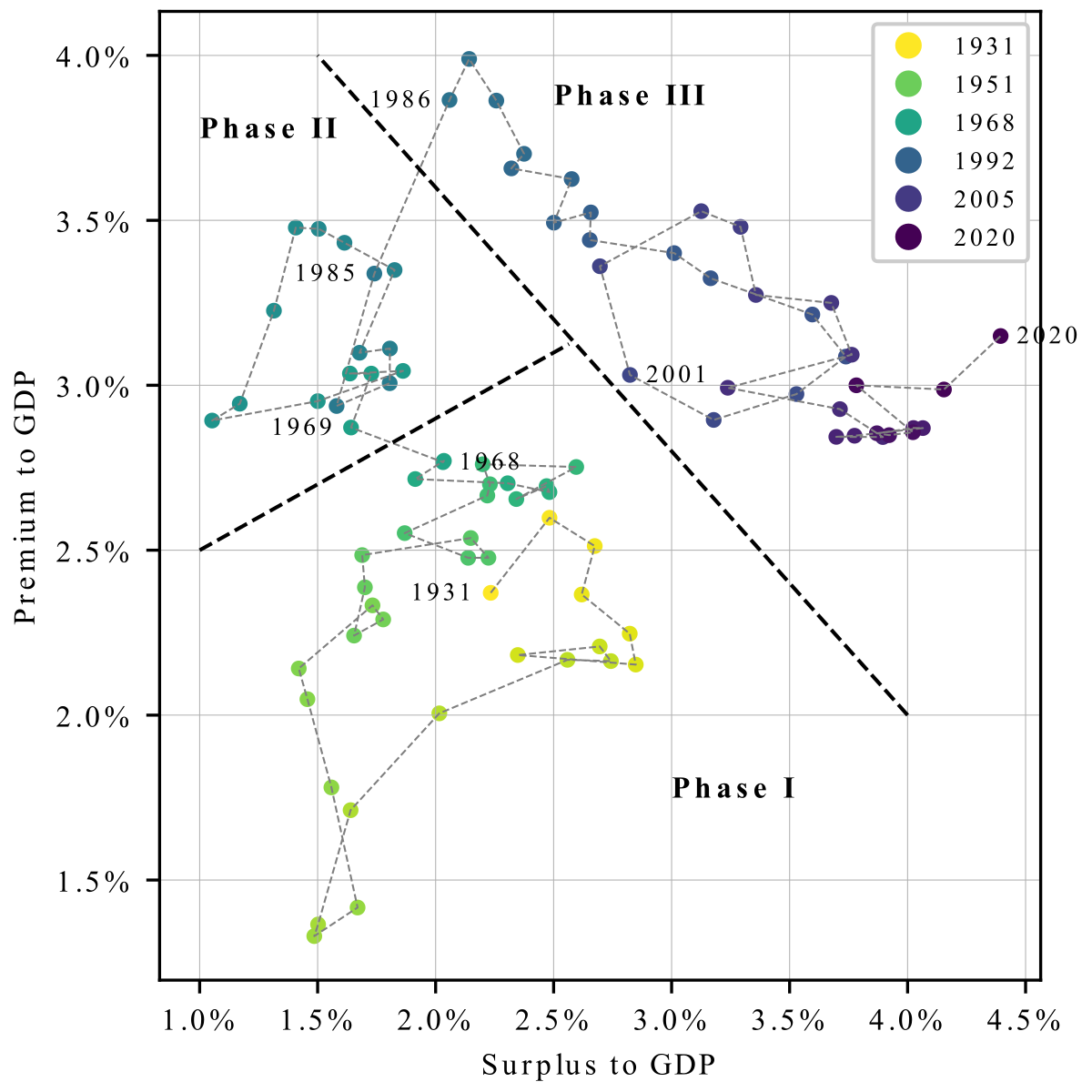

Surplus to GDP Ratio, 1931-2020e

Market Dynamics Since 1986 Explained by Prior Year Surplus Levels

:::::: :::

::: :::

::: ::::::

Direct Loss Ratio Time Series by Major Line

Loss Ratio Time Series by Major Line

Title decoder: CMP; SD=0.111 (0.0661), cor=0.915 ar fit, r2=0.268, rse0=0.089

- Line; standard deviation

- Down-side semi-deviation is shown in parenthsis (explain)

- Correlation of the line with total on the first line

- (second line) shows the \(R^2\) and residual standard error of an autoregressive loss ratio model

Interpretation

- When the

rseis much lower thanSDit suggests the market cycle is predictable - Tends to occur in casualty lines (e.g., commercial auto, medical malpractice, private passenger auto, and workers compensation)

- The cycle for property lines tends to be idiosyncratic, for obvious reasons.

Line Legend

- Thin gray line in each plot shows the

totalloss ratio, for context - The horizontal lines show the mean (thicker) and mean \(\pm \Phi^{-1}(22/23)= \pm1.71\) standard deviations

- If the loss ratios were normally distributed we expect all observations from 22 years (1996-2017) to fall within these tram lines

- They provide a surprisingly good estimate of the range of loss ratio, except for

Financial Lines(which uses a different tick spacing, note).

Direct Loss Ratio Time Series by Major Line, Loss Ratio Scale 0 to 150 Percent

Some Lines Are More Volatile Than Others…

Direct Premium and Loss Dynamics

posted 2021-11-30 | tags: insurance, risk, pricing, presentations